Business and tech innovations Stablecoins: Reimagining money movement for a digital economy

What the data shows:

- Fiat-backed stablecoin purchases on Visa-branded cards outpaced crypto in H2-2025 — average ticket size below $100. The consumer behavior is already on the card rails.

- Retail-sized stablecoin volume for stablecoins USDC, USDT and PYUSD grew from $0.5B to $69.8B between 2019 and 2025 — a 140× increase in six years, with the growth curve steepening.

- Heavy social media use correlates strongly with crypto optimism, with digital-native markets positioned for the fastest adoption. Two in five Gen Z active social media users believe cryptocurrencies are the future of online financial transactions.

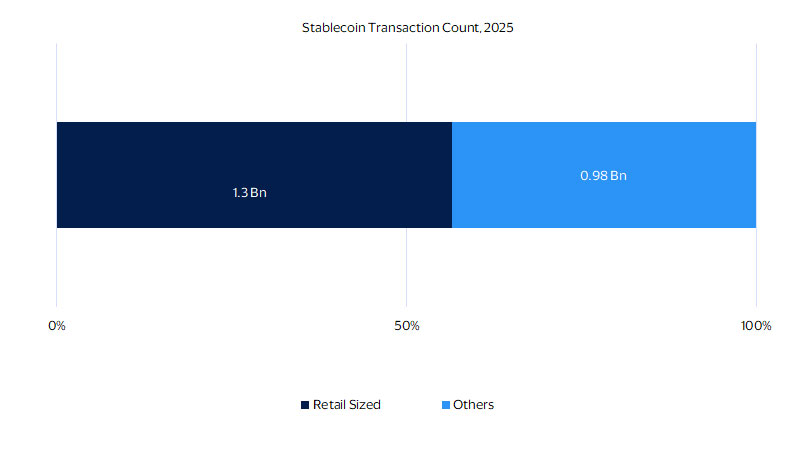

According to the Visa Onchain Analytics Dashboard, the data suggests an increase in retail-sized stablecoin transfers and purchases (transactions below $250), occurring at a frequency similar to everyday consumer spending.¹ Retail‑sized volumes for stablecoins USDC, USDT and PYUSD* climbed from about $0.5 billion in 2019 to $69.8 billion in 2025, roughly matching the size of the Uganda economy. However, this still represents a small portion of global payments; for instance, stablecoins account for around 0.1 percent of U.S. cashless payments.² Over the same period, retail‑sized transaction counts jumped from around 4.7 million to about 1.3 billion. In 2025, retail-sized volume makes up only about 0.6 percent of total adjusted stablecoin volume, but retail-sized transactions account for 57 percent of total transaction count. This reflects a typical pattern you see in consumer payments—that is, many small purchases—signifying that stablecoins could be entering more mainstream use cases (figure below).

That’s why stablecoins have a natural role to play in seamless everyday spend, as well as P2P remittances and B2C payouts, such as cross-border payouts from businesses to creators in emerging markets. Indeed, fiat-backed stablecoin purchases grew faster than crypto purchases in H2-2025, based on VisaNet data.

More than half of all user-initiated stablecoin transactions* are small enough to be ordinary retail transactions

Stablecoin transactions (USDC, USDT, PYUSD) as a share of transactions that exclude automated transactions made by computer programs (bots) in 2025 (percent)

Digital natives are embracing stablecoins

In markets where people shop, chat and pay inside social apps, as well as expect everything to work around the clock, stablecoins tend to catch on fast. Further, consider ecosystems built around super‑apps, creator commerce and cross‑border communities sending money home. In those always‑on, social‑first environments, stablecoins find ready users.

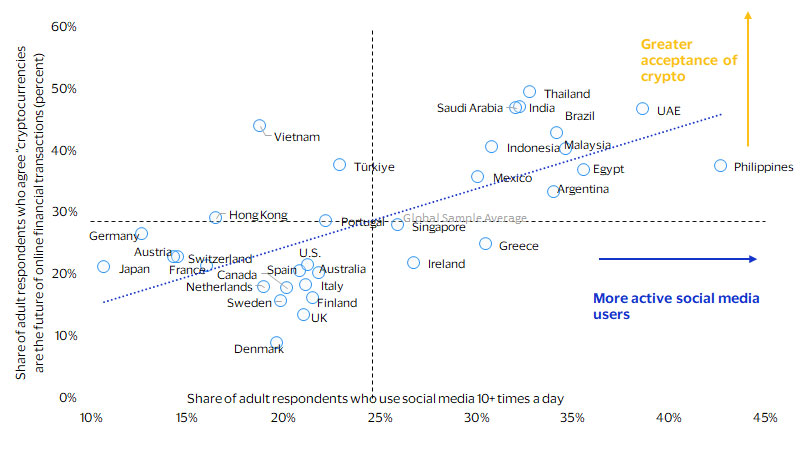

Across countries, belief that “cryptocurrencies are the future of online financial transactions” increases meaningfully with frequent social media use (10+ times/day). The correlation is around 0.7, indicating a strong positive relationship between heavy social media use and crypto optimism (figure below). And as of 2025, two in five Gen Z active social media users believe cryptocurrencies are the future of online financial transactions.³

Consumers are living in a virtual world. In some markets, such as Saudi Arabia, UAE, Brazil and India, consumers surveyed check social 10+ times a day and believe crypto is the future of online financial transactions. These are the markets poised to accelerate consumer adoption of stablecoins faster than ever.

Digital natives will drive early stablecoin adoption

Share of adult respondents who agree “cryptocurrencies are the future of online financial transactions” (percent) vs. share of adult respondents who use social media 10+ times a day (percent)

Stablecoin retail-sized transfers are accelerating

The usage pattern for social commerce, enabled by one-tap checkout, comprises a high volume of small, frequent payments. This matches how stablecoins already show up on-chain, with a larger share of transactions by count. Modest retail-sized stablecoin transfers of USDC, USDT and PYUSD (under $250) are only ~0.6 percent of the dollars moved on a bot-adjusted basis but are ~57 percent of all transactions.⁴

This is particularly evident in PayPal’s PYUSD, a dollar-backed stablecoin built for everyday payments, which has taken off fast. Specifically, retail-sized stablecoin transfers surged from $10,000 USD in 2023 to $3.8 million USD in 2025. Meanwhile, monthly active users jumped from just 15 in November 2022 to about 88,000 by October 2025, and the total supply surged from around $1 million to over $3 billion across Solana and Ethereum blockchains over the same period.

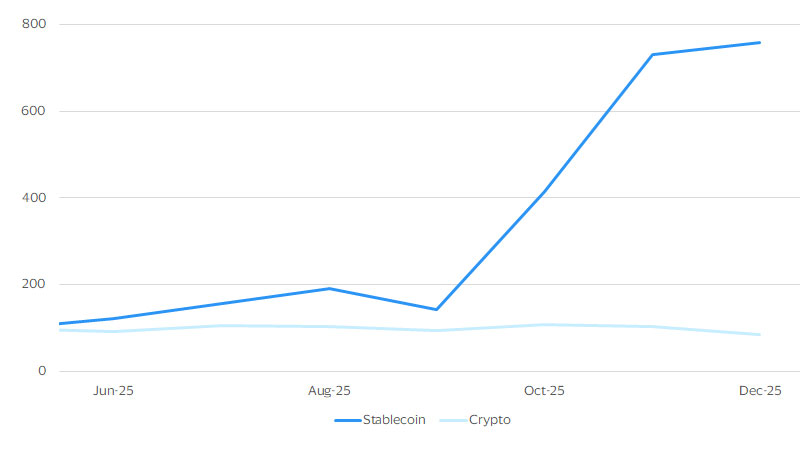

VisaNet data also suggests that purchases of (fiat-backed) stablecoins followed a similar accelerating trend (figure below), outpacing growth of crypto purchases in H2-2025. The average transaction ticket size (excluding B2B transactions) was below $100 at the end of December.

Fiat-backed stablecoin purchases on Visa-branded cards grew faster than crypto purchases in H2-2025

Transaction amount (Index, May 2025=100)

This likely reflects in large part greater regulatory clarity, which makes it easier to plug stablecoins into today’s global payment systems. Specifically, the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, signed into law in July 2025, establishes the first federal framework for regulating “payment stablecoins”—digital assets pegged 1:1 to fiat currency and used for payments. It introduces licensing, reserve, reporting, and consumer protection.

There are significant opportunities for stablecoin adoption in payments over the longer term, beyond the current use cases for stablecoins that revolve around trading and dollar access in the emerging markets. This translates to a massive expansion of total addressable market, such as in cross-border money movement. Countries with meaningful GDP dependence on remittance from migrant workers could seek to utilize stablecoins more and potentially disrupt cross-border banking transactions. Using stablecoins for remittances allows for fast, low-cost cross-border payouts to family and freelancers.

Meanwhile, “agentic” commerce is going mainstream. Gen Z and millennials increasingly let AI recommend, compare and buy, while Asia‑Pacific super‑apps like Grab, GoTo, WeChat, Alipay and Paytm bundle rides, shopping, bill pay and finance under one login. In that setup, a stablecoin-linked payment card can sit behind the same one‑tap checkout, allowing consumers to spend from a stablecoin balance seamlessly at millions of merchants globally—anywhere card payments are accepted—with no change to the user experience. Also, if discovery and purchase happen inside social feeds and chats, stablecoin usage can thrive in the form of creator payouts, instant refunds, micro‑purchases and social media tip jars.

The future of commerce isn’t on the horizon; it’s already here. When we safeguard trust, the positive economics of stablecoins, specifically lower costs and always‑on availability, can accelerate the adoption of stablecoin payments.

Agentic commerce needs always‑on payments

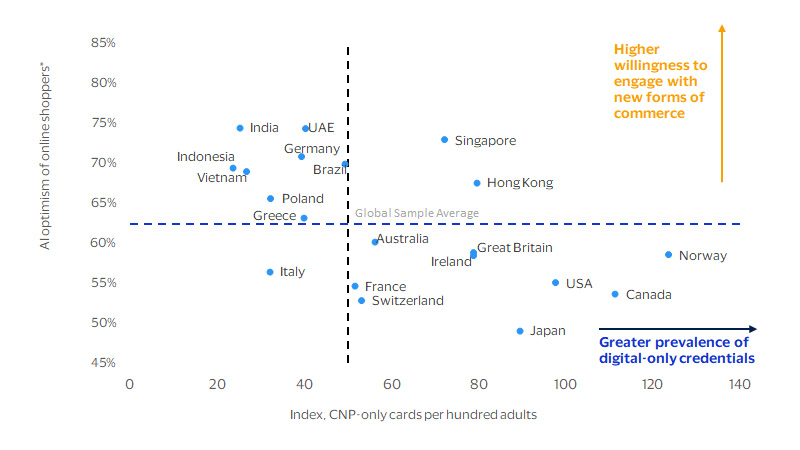

Just as e-commerce needed a digital payment solution, agentic commerce may require new payment solutions that are fast, always-on and programmable—making the long-run opportunity of stablecoins in agentic commerce clear. We’ve already seen the pattern: Commerce is becoming more digital, more social and more “always on.” And the data says the foundation for this shift is already in place. VisaNet data confirms an expanding base of credentials that transact purely via CNP (card-not-present) channels. In some digitally mature markets, digital-only credentials exceed 20 per 100 adults, which represents a mix of consumers who are only transacting online and virtual cards.⁵ Meanwhile, on-chain retail-sized activity continues to accelerate.

Now layer on the next shift: agentic commerce. More shoppers—especially Gen Z and millennials—are getting comfortable letting AI help them research, compare and decide. In fact, as of 2025, one in three Gen Z shoppers now prefer AI platforms (like chatbots or AI search) over search engines or social feeds for product research, a rate that far exceeds older generations.⁶ In the cluster of markets where AI optimism is high, shoppers are ready to delegate: Price‑watching, deal‑hunting and even cart completion can be handled by agents they trust. At the same time, we see a meaningful share of CNP‑only adults. Their default credential lives on file, and their shopping journey is often online. Taken together, these dynamics create some of the fastest on‑ramps for agentic commerce, as seen in markets such as Singapore and Hong Kong (figure below).

So what happens when people move from “AI helps me decide” to “AI completes the purchase for me?”

As payments evolve to agent-led, the foundation for this shift will already be in place

Share of online shoppers who are optimistic about AI (percent) vs. number of CNP-only cards per hundred adults (ratio)

Footnotes

- Visa partnered with blockchain data provider Allium Labs to create the Visa Onchain Analytics Dashboard, a complimentary, user-friendly tool that provides insights into stablecoin growth and activity. The Visa Onchain Analytics Dashboard gives anyone interested in fiat-backed stablecoins more insight into the evolving stablecoin landscape. The dashboard tracks stablecoin movements across 10 major blockchains to highlight trends related to supply and transaction volume and to also address activity. Retail-sized stablecoin transactions refer to transactions below US$250, which could include retail payments, swapping USDC for Ethereum and leveraged trading with USDC.

- U.S. cashless payments are derived from the Bank of International Settlements (latest available 2023 U.S. cashless payments data).

- Based on Visa Business and Economic Insights analysis of YouGov Global Profiles (October 2025).

- The Visa Onchain Analytics Dashboard uses bot-adjusted metrics to provide a clearer picture of stablecoin activity. The methodology involves adjusting for inorganic activity from bots. Details are here: Transactions | Visa Onchain Analytics Dashboard

- Based on an examination of CNP-only cards over a certain period. Further, “CNP‑only” card counts may include virtual cards or additional accounts issued to the same customer. A virtual card is a digital payment credential that functions like a traditional credit or debit card but exists only in electronic form. It is typically issued instantly and can be used for card-not-present transactions. In such cases, online spend may appear on one account while in‑person transactions occur on another, so a “CNP‑only” card does not necessarily indicate a cardholder who shops exclusively online. These factors may influence absolute counts, but it is unlikely to detract from the overall directional trend observed in the analysis.

- 1 in 3 Gen Z and 1 in 4 millennials now turn to AI platforms over other channels for shopping advice, according to new survey from Commerce and Future Commerce

Forward-Looking Statements

This report may contain forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. These statements are generally identified by words such as “outlook”, “forecast”, “projected”, “could”, “expects”, “will” and other similar expressions. Examples of such forward-looking statements include, but are not limited to, statements we make about Visa’s business, economic outlooks, population expansion and analyses. All statements other than statements of historical fact could be forward-looking statements, which speak only as of the date they are made, are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, many of which are beyond our control and are difficult to predict. We describe risks and uncertainties that could cause actual results to differ materially from those expressed in, or implied by, any of these forward-looking statements in our filings with the SEC. Except as required by law, we do not intend to update or revise any forward-looking statements as a result of new information, future events or otherwise.

Disclaimers

The views, opinions, and/or estimates, as the case may be (“views”), expressed herein are those of the Visa Business and Economic Insights team and do not necessarily reflect those of Visa executive management or other Visa employees and affiliates. This presentation and content, including estimated economic forecasts, statistics, and indexes are intended for informational purposes only and should not be relied upon for operational, marketing, legal, technical, tax, financial or other advice and do not in any way reflect actual or forecasted Visa operational or financial performance. Visa neither makes any warranty or representation as to the completeness or accuracy of the views contained herein, nor assumes any liability or responsibility that may result from reliance on such views. These views are often based on current market conditions and are subject to change without notice.

Visa’s team of economists provide business and economic insights with up-to-date analysis on the latest trends in consumer spending and payments. Sign up today to receive their regular updates automatically via email.